Assets vs. Liabilities: The Simple Truth Behind Wealth Building

4/20/20253 min read

Picture a scale. On one side, you've got things that put money into your pocket. On the other, things that take money out. Wealth, in its most elemental form, is a matter of which side weighs more. Understanding the difference between assets and liabilities isn’t just an exercise in accounting — it’s the cornerstone of building a financially secure life.

And yet, it’s one of the most misunderstood concepts in personal finance.

This beginner’s guide unpacks that difference with clarity, relevance, and real-world resonance. Because once you grasp this divide — and act on it — everything else in money management starts to fall into place.

What Are Assets?

They work for you, even when you're not working.

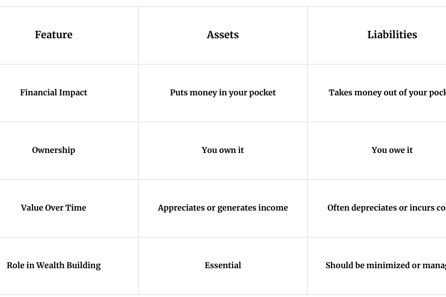

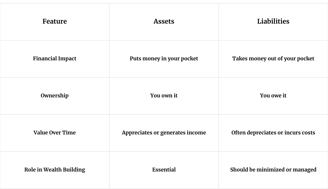

An asset is anything you own that has economic value and can potentially generate income or appreciate over time. In plain English? Assets put money in your pocket — now or in the future.

Think of them as financial seeds. You plant them, and with care, they grow into something fruitful.

Examples of assets include:

Cash and savings accounts

Stocks, bonds, and mutual funds

Real estate that appreciates or produces rental income

A business that generates profit

Intellectual property or royalties

Retirement accounts like a 401(k) or IRA

Some assets are liquid, like cash. Others, like a rental property, are illiquid but may produce long-term cash flow. Either way, they’re part of your wealth-building engine.

What Are Liabilities?

They cost you. And they keep costing you.

Liabilities are financial obligations — debts, payments, or anything that drains money from your pocket. They’re the bills that arrive monthly, the interest that accumulates quietly, the obligations that don’t let you sleep quite as soundly.

Common liabilities include:

Credit card debt

Student loans

Car loans

Mortgages (depending on context)

Personal loans

Unpaid taxes

The irony? Many liabilities look like assets. That shiny new car? It loses value the moment you drive it off the lot. That big house with a giant mortgage? It may be draining your cash flow even if its value appreciates.

Assets vs. Liabilities: Key Differences That Matter

Robert Kiyosaki, author of Rich Dad, Poor Dad, famously said:

“An asset is something that puts money in my pocket. A liability is something that takes money out of my pocket.”

This simple shift in definition reshaped how millions view wealth.

Why This Matters: The Wealth Gap Starts Here

The difference between financially secure individuals and those who struggle isn’t always income. It’s often how they manage the relationship between assets and liabilities.

The wealthy buy assets first, then use the returns to fund their lifestyle.

The poor and middle class often buy liabilities thinking they’re assets (e.g., financing a luxury car as a symbol of success).

It’s not about how much you make. It’s about what you keep — and how you make it work for you.

How to Shift the Balance: From Liability-Heavy to Asset-Rich

1. Track What You Own vs. What You Owe

Start with a personal balance sheet. List your assets and their current values. Then list your liabilities — all debts, monthly payments, and outstanding balances.

Knowing where you stand is the first step to changing direction.

2. Focus on Buying Income-Producing Assets

Don’t just save — invest. Prioritize purchases that have the potential to grow or generate income. This could mean starting a side business, investing in index funds, or buying a small rental property.

Let your money multiply like rabbits, not sit like statues.

3. Avoid Lifestyle Inflation

As your income grows, resist the urge to inflate your lifestyle with liabilities. A higher salary isn’t an invitation to spend — it’s an opportunity to invest.

Live like you're broke — invest like you're rich.

4. Pay Off High-Interest Liabilities First

Debt isn’t always bad, but some of it is toxic. Credit card balances with 20% interest can devour your future. Attack those first — like your financial life depends on it. Because it does.

5. Learn to Recognize False Assets

That timeshare? Liability. That leased luxury car? Liability. That second home you never rent out? You guessed it — liability.

Ask: Does this generate income or value over time? If not, it’s probably not helping you build wealth.

Final Thoughts: Build Your Financial Foundation Brick by Brick

Think of your finances like building a castle. Assets are the stone — strong, sturdy, foundational. Liabilities? They're the termites that eat away at the base when you're not looking.

The difference between assets and liabilities isn’t just accounting jargon. It’s a mindset. A lens through which to see every purchase, every opportunity, every decision. Get it right, and you won’t just survive financially — you’ll thrive.

So ask yourself, every time money leaves your hand:

Is this building me up — or weighing me down?

Contacts

+55 98 9 8137-0224

contact@thefinancenow.com

Subscribe to our newsletter

Your source for finance and business news.

Insights

© 2025. All rights reserved.